Investing in promissory notes presents a compelling choice, given the rapid origination process, enhanced flexibility, and the potential for higher returns compared to other credit funding alternatives. While the ownership of a promissory note is relatively straightforward, navigating the process of selling one can introduce complexities.

For those contemplating the sale of a promissory note, a comprehensive and step-by-step guide becomes an invaluable resource. This guide serves as an essential reference, providing crucial insights and tips that should not be overlooked.

However, before delving into the intricacies of selling a promissory note, it’s prudent to gain a deeper understanding of what a promissory note entails.

What is a promissory note?

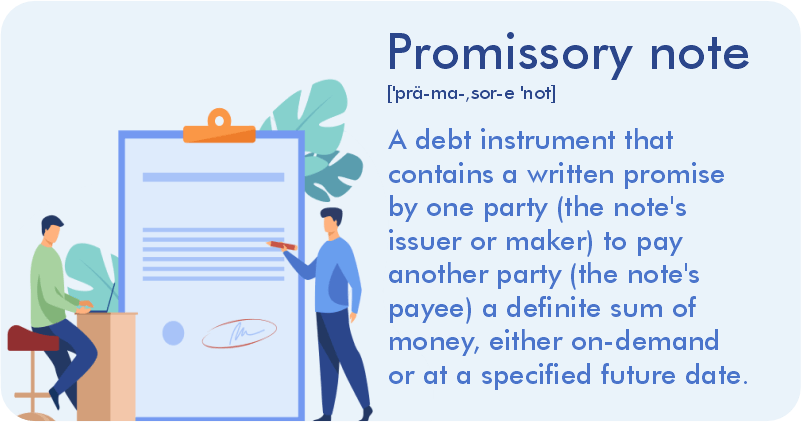

In its simplest form, a promissory note is a legally binding document that encapsulates an unequivocal promise to pay a specified amount of money within predetermined terms, including timeframes and intervals, between two or more parties. The nature of these notes can vary, with some falling under the category of on-demand notes, requiring the borrower to fulfill the payment when formally requested. Additionally, these notes often encompass various terms and conditions that have been mutually agreed upon by the involved parties.

Every promissory note involves distinct roles: an issuer, who is essentially the party making the promise to pay, and a beneficiary, the recipient of this promise. The dynamic between these two roles can manifest in different scenarios, such as a note buyer and seller or a lender and borrower relationship. Understanding these fundamental aspects is crucial before delving into the complexities of selling or transferring promissory notes.

Types of Promissory notes

In its simplest form, a promissory note is a legally binding document that encapsulates an unequivocal promise to pay a specified amount of money within predetermined terms, including timeframes and intervals, between two or more parties. The nature of these notes can vary, with some falling under the category of on-demand notes, requiring the borrower to fulfill the payment when formally requested. Additionally, these notes often encompass various terms and conditions that have been mutually agreed upon by the involved parties.

Every promissory note involves distinct roles: an issuer, who is essentially the party making the promise to pay, and a beneficiary, the recipient of this promise. The dynamic between these two roles can manifest in different scenarios, such as a note buyer and seller or a lender and borrower relationship. Understanding these fundamental aspects is crucial before delving into the complexities of selling or transferring promissory notes.

Why sell a promissory note

Whether you are considering entering the world of promissory note investments or looking to sell an existing note, the optimization of returns is a critical aspect, and the timing of such transactions plays a pivotal role. While the allure of immediate return on investment (ROI) is a common reason for companies to sell promissory notes, there are other compelling motivations for engaging in the sale of these financial instruments.

One significant driver for selling a promissory note is the pursuit of quick recovery. As a debt investment ages, the task of retrieving the invested amount becomes progressively challenging. Older notes tend to depreciate in value over time, and if held for an extended period, the owner may face the risk of incurring losses. Therefore, strategically selling the note at the right moment becomes essential to avoid diminishing returns and potential financial setbacks.

Another noteworthy advantage of selling a promissory note is the opportunity it provides for reinvesting in new notes. By divesting from existing notes at an opportune time, the released capital can be redirected towards fresh investments. This not only facilitates portfolio diversification but also serves to curtail operational costs associated with the recovery of default notes. The ability to reallocate funds efficiently contributes to maintaining a balanced and robust net income for the company.

Furthermore, the sale of promissory notes can help in reducing legal risks associated with the debt recovery process. Traditional recovery methods may become saturated over time, leading to increased legal complexities. However, by placing the promissory note on the market for professional buyers, companies can proactively minimize the legal intricacies involved in recollecting old debts. This forward-looking approach streamlines the debt recovery process and acts as a preventative measure against potential legal challenges, contributing to a smoother and more efficient financial strategy.

What to consider when selling a promissory note?

Be it a personal or commercial promissory note, there are certain factors that one must take into account before selling it. Here’s a step-by-step guide for promissory or mortgage notes sales.

Step 1: Prepare a masked file

Creating an Excel spreadsheet with masked personal information for the borrower of a note involves a meticulous approach to safeguarding sensitive data. This spreadsheet typically encompasses various facets of Personal Identifier Information (PII) while also delving into specific details about the debt. Here’s a comprehensive breakdown of the information to be included:

- Personal Identifier Information (PII): Ensure that any personally identifiable information is appropriately masked to protect the borrower’s privacy. This includes details such as name, address, contact information, social security number, or any other data that could be used to identify the individual.

- Geographical Location of the Debtor: Clearly specify the geographical location of the debtor. This could include the city, state, or any relevant regional information. However, it’s crucial to avoid disclosing specific details that could compromise the borrower’s anonymity.

- Amount of Debt: Provide accurate information regarding the total amount of debt owed by the borrower. This figure should be clearly outlined to give an understanding of the financial obligation associated with the note.

- FICO Score: Include the FICO score of the debtor. The FICO score is a numerical representation of an individual’s creditworthiness, and it plays a significant role in assessing the risk associated with lending. Ensure that this information is masked appropriately.

- History of Payments: Detail the payment history associated with the debt. Include information about when payments were made, any missed payments, and the consistency of the borrower’s repayment behavior. This historical data is crucial for potential buyers assessing the note.

- Judgment Information: If there are any legal judgments related to the debt, provide relevant information in this section. This could include details about court judgments, liens, or any legal actions taken against the borrower. Clearly mask any specific details that could compromise the borrower’s confidentiality.

Maintaining the integrity of the Excel spreadsheet involves employing masking techniques that effectively conceal sensitive information while still presenting a comprehensive overview of the note and the associated borrower. Striking this balance ensures that potential buyers or interested parties can assess the viability of the note without compromising the privacy and security of the individuals involved. Additionally, adherence to data protection regulations and ethical considerations is paramount throughout this process.

Step 2: Prepare all original documentation of the debt portfolio

When it comes to storing media for debt portfolios, two primary methods are commonly employed, each with its own set of considerations. Understanding the nuances of these approaches is crucial for optimizing the sale process and determining the portfolio price effectively.

- Electronic Storage: The electronic storage of media offers a myriad of advantages, influencing both the sale process and the overall portfolio value. When debt portfolios are stored electronically, the sale process tends to be more streamlined and efficient. One of the key advantages is that the buyer gains immediate access to the portfolio after the signing of the Purchase and Sale Agreement (PSA). This immediacy allows the buyer to commence work on the portfolio promptly, contributing to a faster and more dynamic transaction.Additionally, the electronic storage of media contributes to a higher portfolio price. The convenience of immediate access, coupled with the ease of navigating and utilizing electronic files, enhances the perceived value of the portfolio. Buyers are often willing to pay a premium for portfolios that are readily available in electronic format, as it expedites their due diligence and integration processes.

- Hard Copy Storage: In contrast, the storage of media in hard copy format involves the physical documentation being organized and prepared for sale. This typically entails placing the relevant documents in separate boxes, ensuring an organized and accessible presentation. However, it’s essential to note that this method requires additional steps in the sale process.When opting for hard copy storage, the potential buyer may need to request the preparation of media for sale, introducing an additional layer to the transaction timeline. This process may involve sorting, cataloging, and packaging the hard copies for presentation to the buyer.Crucially, before proceeding with the sale of debt portfolios, it is imperative to ascertain the availability of original documentation. The completeness and authenticity of the documentation significantly impact the perceived value of the portfolio and play a pivotal role in building trust between the buyer and seller.

In summary, the choice between electronic and hard copy storage methods can significantly influence the efficiency of the sale process and the ultimate value of debt portfolios. Sellers should weigh the advantages of immediate accessibility in electronic storage against the potential organizational efforts required for hard copy storage, ensuring a strategic and informed approach to portfolio management and sales.

Step 3: Underwriting and closing on a promissory note

Once the necessary paperwork has been generated for both parties involved in the transaction, the subsequent steps typically involve a comprehensive appraisal and title search process for the relevant note and mortgage asset. This critical phase serves to provide valuable insights into the value of the note and mortgage asset, a pivotal consideration for the prospective buyer.

From the buyer’s perspective, understanding the true worth of the note and mortgage asset is imperative. This valuation process involves a thorough appraisal that takes into account various factors such as the property’s current market value, historical performance of the note, and other pertinent considerations. Additionally, a meticulous title search is conducted to ascertain the legal standing of the property, ensuring that there are no encumbrances or issues that could impact its marketability.

Conversely, as a seller, it is crucial to be aware of the buyer’s approach to covering associated costs during this appraisal and title search phase. These costs may include charges for the title search itself, appraisal fees, or expenses related to Broker Price Opinion (BPO). Having clarity on whether the buying party is prepared to bear these costs is an essential aspect of the negotiation process.

The appraisal and title search phase serves as a critical juncture in the transaction, influencing the final decision-making process for both the buyer and seller. For the buyer, it provides a comprehensive understanding of the asset’s value and potential risks, aiding in the formulation of a well-informed investment strategy. On the seller’s end, it offers insights into the buyer’s commitment and financial readiness to proceed with the transaction.

As the appraisal and title search unfold, effective communication between the parties becomes paramount. Open dialogue ensures that any concerns or queries related to the valuation process are addressed promptly, fostering a transparent and collaborative atmosphere. Moreover, understanding the financial responsibilities associated with this phase allows both parties to navigate the negotiation process with a clear understanding of expectations.

In essence, the appraisal and title search phase is a pivotal step in the sale of note and mortgage assets, providing the necessary foundation for informed decision-making and a smooth transition toward the completion of the transaction.

Step 4: Understand each contract

Navigating the intricate landscape of promissory note transactions involves a keen understanding of the terms and conditions outlined in various contractual agreements. Each document plays a pivotal role in shaping the dynamics of the deal, and it is imperative to scrutinize these transaction-related details meticulously. Here are key documents you may encounter throughout the process:

Letter of Intent (LOI): The initiation of a promissory note trade often involves negotiations, culminating in the presentation of a Letter of Intent to the noteholder. This document serves as a formal confirmation of the agreed-upon price and the buyer’s intent to proceed with the purchase. Careful attention should be given to the clauses, including any provisions that grant the note buyer the authority to revoke the price agreement.

Purchase and Sale Agreement: Considered the cornerstone of the transaction, the Purchase and Sale Agreement is a legally binding document that solidifies the commitment of both buyer and seller to complete the trade for the specified promissory note. This comprehensive contract outlines the terms and conditions, ensuring clarity and legal confirmation of the trade agreement.

Commitment Letter: Distinguished from the Purchase and Sale Agreement, the Commitment Letter is a unilateral document that imposes obligations on the note holder. In this agreement, the owner expressly agrees to sell their promissory note at a predetermined price. Understanding the nuances of this commitment is crucial for both parties involved.

Non-disclosure Agreement (NDA): Privacy protection is paramount in promissory note transactions, and the Non-disclosure Agreement serves this purpose. This document stipulates that any information shared during the deal remains confidential, preventing either party from disclosing sensitive details to external entities.

Payout Agreement: Post-closure, the Payout Agreement comes into play, obligating both parties to remit a predetermined amount or percentage of the deal to the broker. This document outlines the terms for compensating the broker for their services after the successful completion of the transaction.

As you navigate the intricacies of promissory note transactions, a thorough examination of these documents is essential for informed decision-making. Whether it’s understanding the implications of a Letter of Intent, cementing the trade through a Purchase and Sale Agreement, committing to the sale with a Commitment Letter, safeguarding confidentiality with a Non-disclosure Agreement, or establishing post-closure financial commitments with a Payout Agreement, each document shapes the trajectory of the transaction and its ultimate success.

Step 5: Close the deal

In the culmination of a promissory note transaction, the final step involves scheduling the closing once all contracts have been meticulously prepared, and due diligence procedures have been adhered to. The intricacies of the agreements dictate that the seller is entitled to receive their payment upon the conclusion of this process, typically within a timeframe ranging from 15 to 35 days.

The closing serves as the ultimate phase, marking the completion of the transaction and the fulfillment of contractual obligations by both parties. During this period, the seller can expect the seamless execution of the predetermined payment terms, bringing the promissory note transaction to its conclusive resolution. This timeline, spanning 15 to 35 days, encapsulates the comprehensive procedures, negotiations, and legal formalities involved in ensuring a smooth and successful closure.

As the closing date approaches, it is imperative for both buyer and seller to remain attuned to the specifics outlined in the agreements, ensuring that all conditions are met, and the transaction is executed in accordance with the mutually agreed-upon terms. This final phase encapsulates the culmination of meticulous planning, transparent communication, and adherence to legal protocols, solidifying the success of the promissory note transaction within the specified timeframe.